TFS Gulf

TFS Gulf

- Deloitte is about to try something incredibly ambitious.

- Starting 1 June 2026, Deloitte consolidates Europe, Middle East, Africa operations under one regional structure called…Deloitte EMEA!

- We’re talking about 80+ countries, 6,000+ partners, & €20Bn+ in revenue.

- Will it work? What does it really mean for clients, partners, and the industry?

Deloitte creates Deloitte EMEA. Why?

On 23 February 2026, Deloitte announced it’s combining 16 major member firms (UK, Germany, France, the Middle East, etc) into one unified structure so they can:

- Align strategy,

- Talent,

- Technology

- Delivery across the region, so cross-border work becomes faster and smoother.

Deloitte’s pitch is simple: Unified structure equals faster delivery.

For instance,

Deloitte’s clients already operate globally. A multinational based in Dubai might need:

- Tax advice in Germany

- Consulting support in the UK

- Technology transformation in South Africa

Ideally, that should feel like one coordinated project. In reality, it can sometimes feel like three separate Deloitte firms negotiating among themselves.

The new EMEA structure is meant to fix that.

At the centre is a €1.5 billion tech investment

Here’s where it gets interesting.

Deloitte plans to pool funds across the region to build:

- Generative AI capabilities

- Sovereign cloud infrastructure (to meet strict EU data laws)

- Industry-specific platforms

Why?

Building serious AI tools is expensive. Individual member firms cannot each build world-class AI on their own.

Pooling resources is the idea.

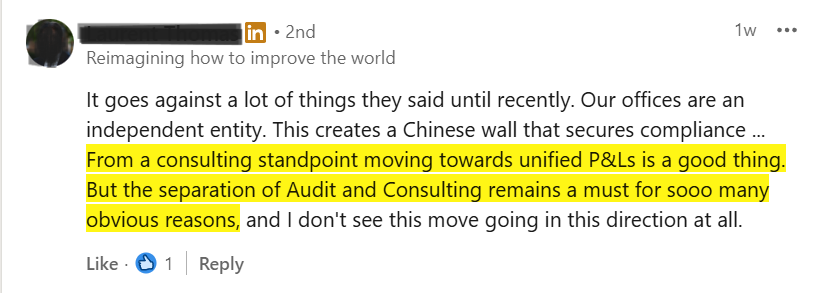

Despite all the talk of unity, liability remains local

The press release explicitly states: “Each participating firm remains responsible for the services it provides within its own market.”

Means? Legal liability stays local.

If a mistake happens in a UK audit, the UK firm is legally responsible, not the entire EMEA entity.

So, despite the branding and total structural consolidation of all service lines across the participating firms…Deloitte EMEA won’t be one legal firm!

So what is actually merging?

Not everything.

- Leadership: Single coordinated regional structure

- Strategy: Shared playbook

- Technology: Centralised investment and platforms

- Delivery standards: More consistency

But:

- Local legal responsibility remains

- National partnerships still exist beneath the regional umbrella

Example: A UK auditor still cannot sign off on a German company’s books. However, the technology and standards behind the audit may be unified.

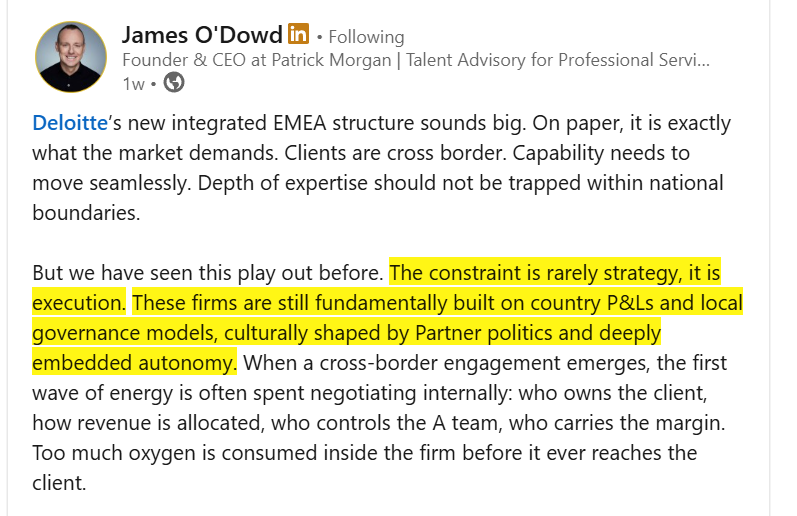

Why partner politics matters?

James O’Dowd (Founder, Patrick Morgan) delivered a viral critique on LinkedIn, noting that while strategy is easy to announce, execution is the “constraint.”

He warns that firms are still culturally built on “country P&Ls” and partner politics.

And argues that too much “internal oxygen” may be wasted negotiating:

- Which team owns the client?

- How is revenue shared?

- Who leads delivery?

- How are margins allocated?

If those questions take too long to answer, energy is spent within the firm rather than solving problems for clients.

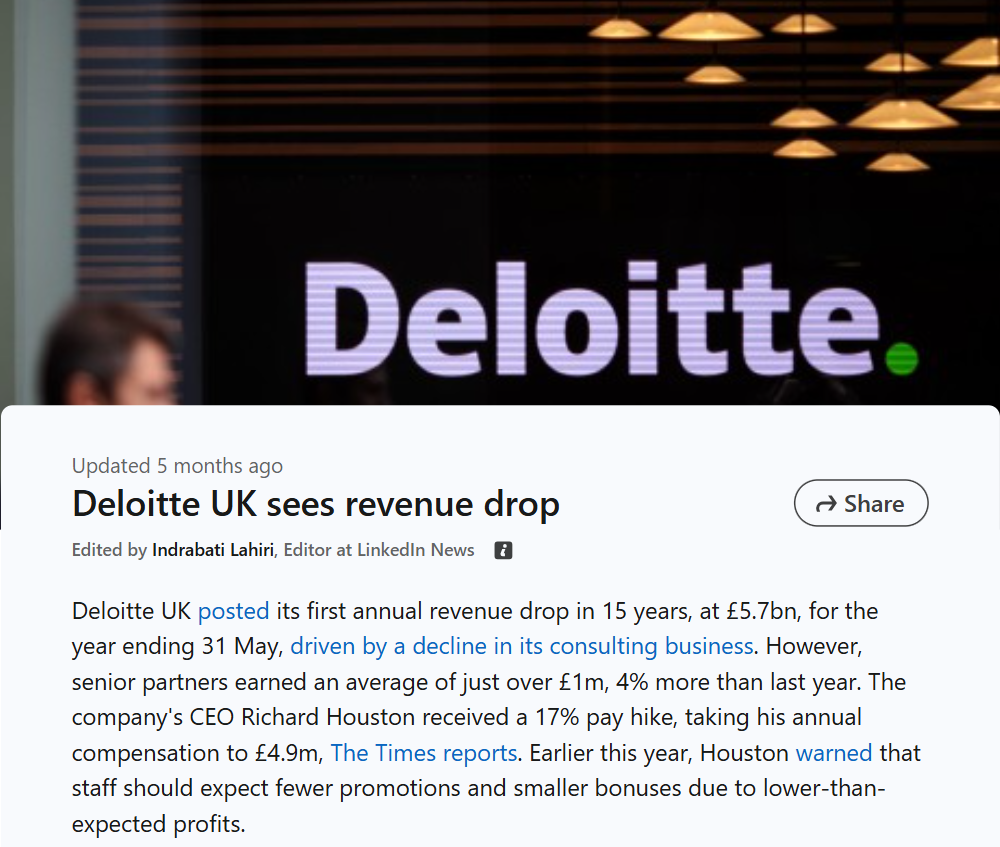

Also read: KPMG merging several of its individual country practices

Also read: KPMG forced Auditor for a 14% AI Discount…Will the “Billable Hour” die?

What is social media saying?

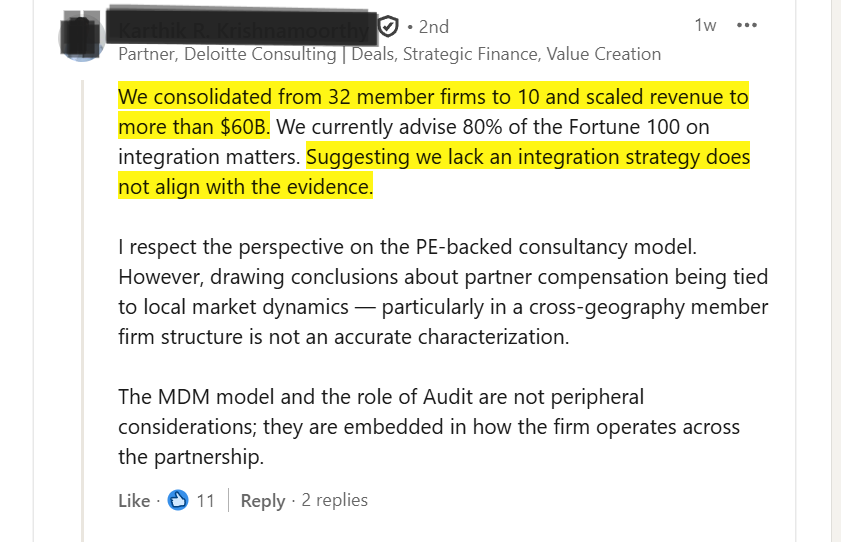

In a LinkedIn conversation thread, a Deloitte US Consulting Partner points to the evidence:

“Professional services firms are not newcomers to integration. They have evolved over decades to meet client demand.

Deloitte has already scaled from 32 member firms to 10 and reached $60B in revenue.”

He dismisses critics as “Monday morning quarterbacks pontificate on a firm strategy based on conjecture and no inside information,” and insists the partners voted for this change.

Dritan Saliovski (M&A Advisory) agrees, noting that the “One Firm” pitch is a powerful sales tool that wins massive cross-border mandates. For many, this is simply the evolution required to meet modern client demands.

Some industry voices believe…

This move is less about efficiency and more about “Deloitte’s survival”.

A few transformation specialists mentioned,

“Audit / advisory revenue will be wiped out 50% by AI… If Deloitte doesn’t use this €20B scale to build proprietary tools, they are stuck selling “daily man-hours,” a game they are destined to lose in an automated world.”

Wrapping up….

As of June 1, 2026, the leadership is set:

- CEO: Richard Houston (currently CEO of Deloitte North & South Europe and Deloitte UK)

- Deputy CEO: Volker Krug (Deloitte Germany)

- Chair: Sami Rahal (Deloitte Central Europe)

- Deputy Chair: Liesbeth Mol (former Chair of North & South Europe)

Joe Ucuzoglu, CEO of Deloitte, described the EMEA merger as a “historic moment” for the company.

But many questions remain:

Will Deloitte successfully combine scale, technology, and regional coordination to reshape professional services?

Will Deloitte become a product business?

Will pooling resources (for AI and technology) necessarily mean pooling all profits?

The professional services industry is built on partnerships and local autonomy. How will ” partner profits ” be shared under the new EMEA structure?

FAQs:

Which countries are part of Deloitte EMEA?

Internally, the region consists of five major clusters that combine geographies with similar market dynamics:

- UK & Ireland

- North & South Europe

- Central Europe

- Middle East

- Africa